Short-term insurance explained: what car, home, contents and buildings cover protects, what it costs and how to choose the right cover in South Africa.

Your car gets stolen. Your geyser bursts and floods half the house. Someone bashes your bumper in peak traffic, and suddenly your monthly budget has flown out the window, leaving you with some very expensive bills.

That's usually when people start paying attention to short-term insurance.

For a lot of South Africans, insurance feels like one of those things you know you should understand… but somehow never quite get around to until something expensive goes wrong.

So let's fix that, with a clear, practical breakdown of how short-term insurance works in South Africa, what it covers, what affects the cost and whether it's actually worth it.

What is short-term insurance?

Short-term insurance covers the things you own against risks like theft, accidents, fire, storm damage and other unexpected events. Think cars, homes, household contents and valuables.

You pay a monthly premium. In return, your insurer agrees to cover certain financial losses if something listed on your policy happens. If you claim and the event is covered, they'll pay for repairs, replacement or damages, minus your excess.

An excess is the amount you pay towards a claim before the rest is covered.

It's called "short-term" because policies are typically renewed every year (even though you pay monthly). It's also flexible, so you can update or cancel your cover as your life changes.

What does short-term insurance cover?

The main personal short-term insurance products are usually car insurance, home contents insurance, buildings insurance, and cover for specific valuables you take out of the house, like phones, laptops, jewellery, bicycles or cameras.

Car insurance

Car insurance can cover damage to your car, theft, accidents and damage you cause to someone else's vehicle or property. There are usually three main types of car insurance:

Comprehensive cover gives you the broadest protection. It can cover damage to your own car, theft, hijacking, accidents, and damage you cause to someone else's vehicle or property.

Third-party, fire and theft cover is more limited. It can cover damage you cause to others, as well as loss or damage to your car from fire or theft, but it usually won't cover accident damage to your own car.

Third-party only cover mainly protects you if you damage someone else's car or property. It won't usually cover your own car.

That difference matters. If you rely on your car every day, choosing the right level of cover can make a big difference when something goes wrong.

In South Africa, this is a big one. Vehicle theft, hijacking and road accidents are real risks, and one bad day on the road can cost far more than most people have sitting in savings. According to SAPS, around 85 vehicles are stolen every day, and that is before you count hijackings, which SAPS records separately.

Home contents insurance

Home contents insurance covers the stuff inside your home. That means things like TVs, laptops, phones, appliances, furniture, clothes and other belongings.

This is especially useful if there is a break-in, fire, flood or burst pipe. Break-ins are an everyday risk for many South African households. Just check your policy carefully, because some high-value items may need to be specified separately.

Specified items

Some valuable items need their own cover, especially if you regularly take them out of the house.

Think phones, laptops, watches, engagement rings, bicycles, cameras or other expensive items you carry around with you. Your home contents cover may protect these items while they are inside your home, but not necessarily when you take them out.

So if you want them covered when you're out and about, check whether they need to be specified separately on your policy.

Buildings insurance

Buildings insurance covers the actual structure of your home.

That includes things like walls, the roof, floors, permanent fixtures, built-in cupboards and sometimes garages or boundary walls, depending on your policy. It can protect you against events like fire, storms, flooding and other damage to the building itself.

Liability cover

Short-term insurance can also protect you if you are legally responsible for damage to someone else's property.

For example, if you cause an accident and damage another person's car, or something at your home causes damage to a neighbour's property, you could be responsible for the cost.

That kind of bill can be a nasty financial shock, which is why liability cover is an important part of short-term insurance.

What does short-term insurance usually not cover?

Every policy has exclusions, and knowing them upfront saves you a nasty surprise at claim stage. Short-term insurance generally won't cover:

- Wear and tear, ageing and gradual deterioration

- Mechanical or electrical breakdown, or damage from poor maintenance

- Deliberate or reckless damage

- Damage caused while driving under the influence or without a valid licence

- Using your car for something it isn't insured for, like e-hailing or business use when you're only covered for private use

- An unroadworthy vehicle, for example bald tyres

- Consequential or indirect losses

The specifics live in your policy wording, so it's worth a read before you need it.

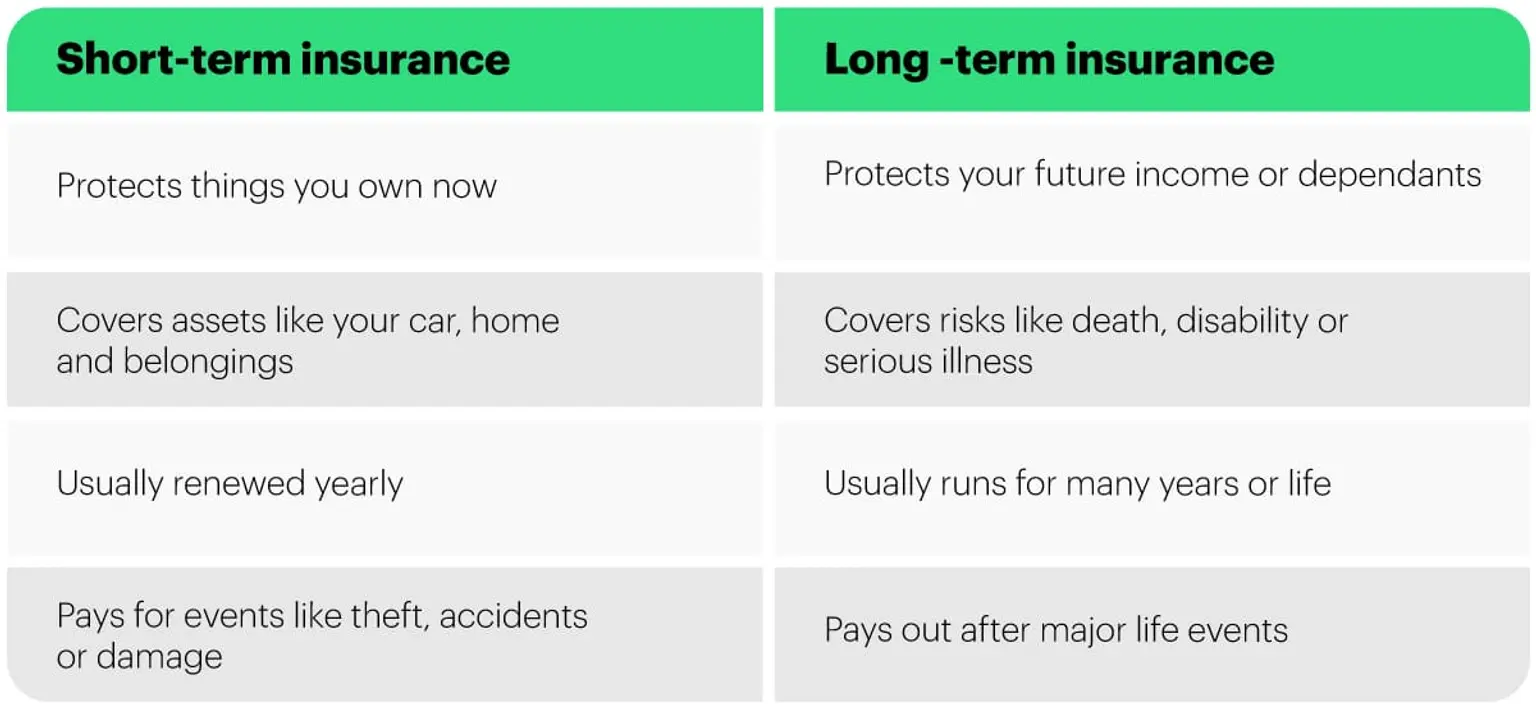

Short-term insurance vs long-term insurance

This is one of the most common questions. Here's a simple breakdown:

So, short-term insurance protects your stuff. Long-term insurance protects your future financial security and the people who rely on you. Different jobs, same general idea: reducing the financial damage when life gets messy.

Is short-term insurance worth it in South Africa?

It's not really about whether it's worth it. The question you should be asking is whether you could afford to recover on your own financially if something went badly wrong.

- Could you replace your car if it was written off tomorrow?

- Could you replace your laptop, TV and furniture after a break-in?

- Could you rebuild part of your home after a fire or flood?

If the answer is no, insurance helps you avoid carrying that full financial risk yourself.

Some people can self-insure smaller losses, like replacing a phone or fixing minor damage. But bigger losses are harder to absorb. That's where short-term insurance can make the difference between an annoying setback and a financial disaster.

Why are so many South Africans uninsured or underinsured?

South Africa is underinsured, which means many people either have no insurance or don't have enough cover.

There are a few reasons for this:

- Insurance can feel expensive

- Policies can be confusing

- People worry claims won't be paid

- Many assume "it won't happen to me"

- Some choose lower cover just to reduce the monthly premium

The problem is that underinsurance usually only shows up when you claim.

For home contents, it could mean your furniture, appliances, electronics, clothes and other belongings cost more to replace as new than the amount you insured them for.

For buildings insurance, it could mean your home is insured for less than it would actually cost to rebuild. This is where many people get caught out: your building should usually be insured for what it would cost to rebuild, not what you could sell it for. Market value and rebuild cost are not the same thing.

And for specified items, it could mean an expensive phone, laptop, bicycle, watch or piece of jewellery was never added properly, or was not covered away from home.

Not fun. Very avoidable.

A good rule is to review your cover regularly and ask: "If I had to replace or rebuild this today, would my cover be enough?"

Common misconceptions about short-term insurance

"Insurance covers everything."

Nope. Insurance covers specific risks listed in your policy, and every policy has exclusions. If you're not sure what yours are, the section above is a good place to start.

"The cheapest premium is always best."

A lower monthly premium can be tempting, but check what you're trading away. It might mean a higher excess, lower limits or less cover. Cheap insurance can get very expensive if it doesn't help enough when you claim.

"My valuables are covered everywhere."

Not always. Phones, laptops, jewellery and other valuables may need extra cover if you take them out of your home regularly.

"If I never claim, I wasted my money."

Insurance isn't an investment. It's protection. Ideally, you never need it. But if you do, you'll be very glad it's there.

"All policies are basically the same."

They're really not. Cover, exclusions, excesses, claim processes and customer experience can differ a lot. Read the details before you decide.

What is an excess in insurance?

Your excess is the amount you pay towards a claim.

For example, if your car repairs cost R30,000 and your excess is R5,000, you pay the first R5,000. Your insurance provider covers the remaining R25,000, as long as the claim is covered.

A higher excess can lower your monthly premium. A lower excess usually means a higher monthly premium.

The trick is choosing an excess you could actually afford in an emergency. A low premium is great until your excess gives you a small heart attack.

How to choose the right short-term insurance

Know what you own

Make a simple list of your belongings and what they'd cost to replace today. This helps you avoid underinsuring yourself.

Don't only compare premiums

Look at the full picture: cover, limits, excesses, exclusions and claim experience.

Check what's excluded

This is where most surprises hide. Know what your policy doesn't cover before you need to claim.

Think about claims

When something goes wrong, you want a claims process that's fast, clear and low on admin. Price matters, but so does the experience when you actually need help.

Review your cover regularly

Your insurance should keep up with your life. Update it when you move, renovate, buy expensive items, change cars or realise your stuff is worth more than you thought.

So, where does that leave you?

Short-term insurance may not be thrilling dinner-party material. Fair.

But it is one of the more practical financial decisions you can make.

In South Africa, risks like theft, accidents, fire, floods and storm damage are part of real life. The right cover helps you recover without having to drain your savings, take on debt or start from scratch.

The right cover should be easy to understand, easy to update, and there when you need to claim. That's the part Naked is trying to make simpler: a quote in minutes, cover you can manage in the app, and a claims process designed to be fast and low-admin.

Get covered in about 90 seconds

Whether it's your car, your home, the contents inside it or the things you carry every day, Naked lets you quote and buy in minutes, and manage it all from the app.

Jump straight to what you need: car insurance, home contents insurance, buildings insurance or single item insurance.